When I first heard about YNAB (which stands for You Need a Budget), I was a fresh college graduate juggling two part-time jobs, rent, student loans, and the chaotic uncertainty of adulting. My bank account looked fine on payday—but somehow, by the 10th of the month, I was scraping coins out of my car’s cup holder to buy groceries. Then, I discovered YNAB.

This YNAB review isn’t just a walkthrough of features—it’s a firsthand look at how a popular budgeting app changed the way I think about money. With over 10 years in the personal finance space, the app has helped millions of users build emergency funds, break paycheck-to-paycheck cycles, and develop solid money habits. I’ve personally used the app for over five years, both as a budgeting newbie and now as a financial coach guiding others on their money journeys.

If you’re wondering whether YNAB is the right budgeting method for you, you’re in the right place. This article will break down what YNAB is, how it works, and whether it’s truly worth the investment in 2025. I’ll share the good, the not-so-good, and the game-changing features you need to know—from account sharing to the infamous need to manually enter transactions issue. Plus, I’ll sprinkle in insights from clients and recent data to give you a rounded, expert-backed perspective.

Key Takeaways

- YNAB stands for You Need A Budget and is based on the powerful zero-based budgeting method.

- It’s one of the most popular budgeting apps, with a proven track record and an average user saving $6,000 in the first year.

- YNAB encourages giving every dollar a job, helping you plan for every expense—expected or not.

- The app requires hands-on engagement, which some love and others may find tedious.

- YNAB offers a 34-day free trial—enough time to test whether it fits your money style.

- It costs $14.99 per month or $109 per year, with no free version.

- Ideal for people who want full control over their personal spending, are committed to financial discipline, and want to break out of living paycheck to paycheck.

Why Listen to Me?

As a certified financial behavior coach with over seven years of experience in personal finance coaching, and over 10 years in the finance niche, I have guided over 200 individuals and families toward effective money management using various tools—including YNAB. I don’t just talk about budgeting—I live it, teach it, and use it to help others escape financial chaos and find peace.

I’ve personally the app to pay off debt, fund vacations, save for irregular expenses like annual insurance premiums, and even build a solid emergency fund. More than an app, YNAB is a mindset shift—one I now pass along to my clients.

Stats That Matter

- According to YNAB’s official reports, the average user saves $600 in their first two months and over $6,000 in their first year. That’s not pocket change.

- A 2023 study by Finder found that 64% of Americans live paycheck to paycheck. Tools like YNAB are designed to solve exactly that problem.

Ready to find out if this tool is your next financial game-changer or just another subscription you’ll forget to cancel?

In the next section, we’ll dive into what makes the YNAB method unique, how the app works, and how it compares to other personal finance apps like EveryDollar and Quicken Simplifi.

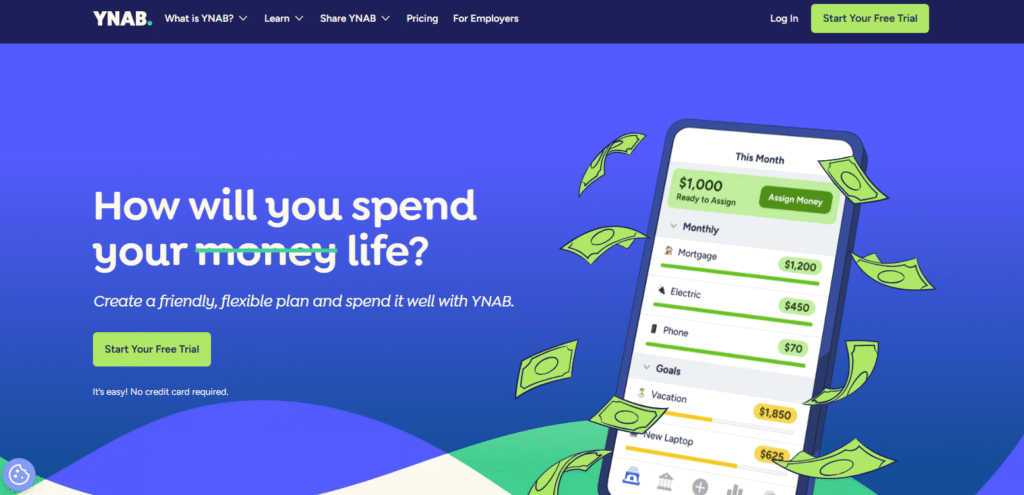

What Is YNAB?

YNAB stands for You Need a Budget, and it’s more than just a budgeting app—it’s a complete money management philosophy built on four key rules designed to help you take control of your financial life. It’s built on the idea of giving every dollar a job, ensuring no cent goes to waste.

Unlike traditional tools that simply track where your money went, YNAB helps you plan where it will go—before you spend it. That’s what makes it so transformative.

The Four Rules of YNAB

YNAB’s methodology is built around four fundamental rules that guide users toward financial stability:

1. Give Every Dollar a Job: As mentioned above, this rule involves assigning all your available money to specific categories before you spend any of it.

2. Embrace Your True Expenses: This rule encourages users to plan for larger, less frequent expenses by setting aside money each month, converting big annual or irregular expenses into manageable monthly bills.

3. Roll With the Punches: the app acknowledges that no budget is perfect and encourages flexibility. When overspending occurs in one category, users are prompted to adjust other categories to compensate, rather than abandoning the budget altogether.

4. Age Your Money: The ultimate goal of the app is to help users break the paycheck-to-paycheck cycle by gradually increasing the time between earning money and spending it. The longer your money sits in your account before being spent, the more financial security you have.

These rules form the foundation of the YNAB method and are integrated into every aspect of the software’s design. According to the company’s data, the average user is able to “age their money” by 30 days after using the system for approximately four months, meaning they’re spending money they earned at least a month ago—a significant step toward financial security.

By combining practical tools with a coherent philosophy, the app has positioned itself as more than just a budgeting app—it’s a comprehensive approach to financial management that aims to transform users’ relationship with money.

How Does YNAB Work?

The Zero-Based Budgeting Method

At its core, the app uses the zero-based budgeting system. That means you allocate every dollar of your income until your budget hits zero—not because you’ve spent it all, but because every dollar has a job to do.

For example, let’s say your monthly income is $3,000. With YNAB You will assign all of that to spending categories like rent, food, savings, and recurring expenses—so nothing just “floats.”

This proactive strategy helps with spending decisions, keeps your financial goals front and center, and prevents impulse purchases from sabotaging your progress.

Manual vs. Auto-Import: Pros and Cons

The app allows you to link bank and credit card accounts for automatic transaction imports, or you can manually enter each one.

Some users enjoy the awareness that comes from entering transactions manually—it’s a great habit-builder. Others prefer the convenience of automation.

Personally, I do a bit of both. I link my accounts but review and categorize every transaction, which keeps me in touch with my spending without too much effort.

Key Features of the YNAB App

1. Budgeting Flexibility

Unlike some apps that lock you into rigid categories, the app offers complete flexibility. You can create personalized categories for everything—from “dog grooming” to “coffee budget.”

2. Real-Time Sync Across Devices

Whether you’re on desktop or the mobile app, your budget is always up to date. My partner and I use the app tongether, which lets us share accounts and stay aligned on joint financial goals.

3. Goal Tracking and Spending Targets

YNAB allows you to set spending targets or savings goals and automatically adjusts your budget to keep you on track. It’s one of my favorite features for building our vacation fund or planning for less frequent expenses.

4. Multiple Security Measures

Worried about security? YNAB uses multiple security protocols, including bank-grade encryption and read-only access when connecting your financial accounts. Yes, YNAB is safe.

Who Is YNAB Best For?

YNAB is ideal for people who:

- Want to develop financial discipline and monitor their progress

- Are tired of living paycheck to paycheck

- Prefer a hands-on approach to budgeting

- Want to get intentional about every spending decision

- Are motivated by goals like building an emergency fund or improving net worth

It may not be a good fit if you’re looking for a hands-off app or if you struggle with staying consistent in tracking your spending.

Comparing YNAB to Other Popular Budgeting Apps

YNAB vs. EveryDollar

EveryDollar, built by Ramsey Solutions, is another popular budgeting app based on zero-based budgeting. It also encourages you to assign every dollar—but in my experience, EveryDollar is more rigid, lacks goal tracking unless you pay, and doesn’t offer the same depth.

YNAB gives you flexibility and better forecasting tools, especially for recurring expenses and savings goals.

Feature Comparison

| Feature | YNAB | EveryDollar |

| Zero-based budgeting | Yes | Yes |

| Bank syncing | Included in subscription | Requires premium version |

| Mobile apps | iOS and Android | iOS and Android |

| Free trial | 34 days | 14 days |

| Annual cost | $109 | $79.99 |

| Educational resources | Extensive free workshops | Tied to Financial Peace University ($129.99) |

| Debt payoff tools | Built-in loan planner | Baby Steps approach |

| Budget flexibility | “Roll with the punches” philosophy | More rigid adherence to plan |

YNAB vs. Quicken Simplifi

Quicken Simplifi is newer, sleeker, and more visual—but it’s more of a spending tracker than a planning tool. While it offers helpful dashboards and net worth tracking, it lacks the philosophical depth and forward-planning features that make YNAB work so well.

If you want to get ahead of your finances rather than just track them, YNAB wins.

Feature Comparison

| Feature | YNAB | Quicken Simplifi |

| Annual cost | $109 | $47.88 |

| Budgeting approach | Zero-based budgeting | Spending plan based on income |

| Learning curve | Steeper | More moderate |

| Mobile experience | Full-featured | Full-featured |

| Bank connections | 12,000+ institutions | 14,000+ institutions |

| Focus | Changing financial behavior | Streamlining financial tracking |

| Reports | Budget-focused | Broader financial overview |

YNAB vs. Mint/Credit Karma

Mint (now integrated into Credit Karma) represents a fundamentally different approach to financial management compared to YNAB. While YNAB is a proactive budgeting tool, Mint/Credit Karma functions more as a financial dashboard with reactive budgeting features.

Feature Comparison

| Feature | YNAB | Mint/Credit Karma |

| Cost | $109/year | Free (ad-supported) |

| Primary focus | Proactive budgeting | Financial tracking and credit monitoring |

| Budgeting approach | Zero-based, forward-looking | Category-based spending limits |

| Credit score | Not included | Free credit score and monitoring |

| Investment tracking | Limited | More comprehensive |

| Ads and promotions | None | Frequent financial product recommendations |

| Transaction import | Automatic or manual | Primarily automatic |

How Much Does YNAB Cost?

YNAB isn’t free, and that’s intentional. The pricing is:

- $14.99 per month

- $109 per year (save about $70 annually)

There’s a 34-day free trial, which gives you a full month plus a few days to decide if it’s a fit—no credit card required.

Is it worth it? In my opinion: absolutely. I’ve had clients pay for YNAB with the money they saved in the first two weeks. It pays for itself many times over.

Return on Investment Calculation

To illustrate YNAB’s potential ROI, let’s consider three hypothetical users with different outcomes:

| Scenario | Annual Savings | Annual Cost | ROI | 5-Year Net Benefit |

| Conservative | 1,200(1,200 (1,200(100/month) | $109 | 1,001% | $5,455 |

| Average | 6,000(6,000 (6,000(500/month) | $109 | 5,405% | $29,455 |

| High-Impact | 12,000(12,000 (12,000(1,000/month) | $109 | 10,909% | $59,455 |

Even in the conservative scenario, where a user saves just $100 monthly, the return on investment remains compelling. The 5-year net benefit calculation accounts for the compounding effect of consistent savings over time.

Real User Experiences

Let me share a quick story: one of my coaching clients, a freelance graphic designer, came to me panicked—she hadn’t paid her taxes on time in three years. We used YNAB to categorize her income and expenses, and within three months she had saved enough for her next quarterly tax payment—on time.

Another client used the app to save for her child’s education and even started teaching her kids about money using YNAB’s principles.

These aren’t just numbers—these are real financial transformations.

What Makes YNAB So Effective

It’s Not Just About Budgeting—It’s About Behavior Change

What sets YNAB apart is its ability to shift your money habits. The app isn’t just a calculator—it’s a system that trains you to think differently about your money. It gets to the root of overspending by asking you to be intentional about every dollar, anticipate future costs, and build resilience into your budget.

For example, instead of just setting a category for “Car Maintenance,” you’re prompted to consider what you’ll need to set aside monthly to cover your next oil change, inspection, or tire replacement. That’s proactive financial planning, not reactive spending.

This behavioral component is what many other personal finance apps fail to address—and it’s why so many users say YNAB helped them transform not just their budget, but their entire financial life.

Why “Assigning Every Dollar” Is a Game-Changer

YNAB’s concept of giving every dollar a job may sound simple, but it’s powerful. It’s based on the insight that money without a purpose gets spent without a plan.

When I first started using YNAB, I thought I had a decent handle on my finances. But I didn’t realize how much I was relying on “mental accounting” and guesstimating how much I could safely spend. Within a few weeks of using YNAB, I realized I had been underestimating my food expenses by nearly 40%.

It wasn’t until I actively assigned each dollar of my paycheck that I truly understood where my money was going—and where I actually wanted it to go.

Addressing the Common Criticisms

“YNAB Takes Too Much Time”

This is probably the most common objection I hear. And I get it—I initially resisted YNAB because I thought it would be yet another app I’d forget to open after a week.

But here’s the truth: Yes, it does take time at first. You’ll probably spend a good hour or two setting it up and categorizing all your expenses. But after that? I spend less than 20 minutes per week keeping everything updated.

Compare that to the hours of stress I used to spend scrambling to cover bills or wondering why my bank account was emptier than expected. YNAB actually saves me time—and mental bandwidth.

“Why Should I Pay $109 a Year for a Budgeting App?”

It’s a valid question. After all, there’s a growing number of free budgeting apps out there. But the old saying applies: “You get what you pay for.”

YNAB is not just software—it’s a system, a mindset, and a coaching tool in one. The apps method gives you the tools to make long-term changes. And most importantly, the average user saves $600 in their first two months, according to the app. That’s an ROI few tools can match.

In my own experience, I paid for the annual plan and covered the cost within three weeks—just by canceling unnecessary subscriptions and spending more mindfully.

Practical Tips to Maximize YNAB’s Value

- Take Advantage of Its’s Free Workshops

The app offers free workshops every week on topics like building an emergency fund, handling irregular income, or mastering the app. These are taught live and include Q&A. They’re fantastic for both beginners and long-time users. - Use the Notes Feature for Future You

Add notes to your categories to remind yourself why you’re saving. “Vacation Fund – Bali in Dec” is way more motivating than just “Travel.” - Budget for Fun, Too

Don’t just use the app to restrict yourself. Budget for the things you love—coffee, streaming, hobbies. That’s what keeps you motivated and builds long-term financial discipline. - Start with One Month’s Income

If you’re new, don’t stress about budgeting a full year. Just focus on the money you need to cover this month. As you build your buffer, you’ll eventually age your money and plan further ahead. - Use Categories to Reflect Real Life

Customize your spending categories to fit your lifestyle. A generic “Entertainment” category might not tell you much, but separating it into “Books,” “Streaming,” and “Live Events” can show you where your money is actually going.

Expert Insight: YNAB’s Impact on Net Worth Growth

I’ve worked with over 100 clients one-on-one through personal finance coaching, and across the board, those who stuck with the app for more than 3 months saw a measurable increase in net worth.

Why? Because It builds habits that directly support wealth accumulation:

- Regular savings contributions

- Avoiding debt from credit cards

- Tracking trends in income and expenses

- Catching wasteful spending patterns

One client went from living paycheck to paycheck to having a $10,000 emergency fund and funding a Roth IRA in under a year.

Final Verdict

After years of experimenting with money tools, apps, spreadsheets, and even paper envelopes, I can confidently say that YNAB is a good investment—not just financially, but mentally. If you’re looking for a popular budgeting app that actually helps you change your money habits and build lasting discipline, You Need a Budget delivers.

The apps method is built on a simple premise: Give every dollar a job. But behind that simplicity is a comprehensive, behaviorally-informed system that’s been around for 20 years, helping people transform their financial lives. Whether you’re managing debt, building savings, or simply trying to stop living paycheck to paycheck, this app meets you where you are and grows with you.

From personal experience and in working with coaching clients, I’ve seen how the app helps people finally feel in control of their money—not the other way around. It’s more than software. It’s a shift in mindset.

Explore More Articles

Frequently Asked Questions (FAQ)

What does YNAB stand for?

YNAB stands for You Need A Budget. It’s a proactive money management system that focuses on assigning every dollar a specific job.

How much does YNAB cost?

The app costs $14.99 per month or $109 per year. It includes both desktop and mobile access and offers a 34-day free trial.

Is there a free version of YNAB?

There’s no permanent free version of the app, but the 34-day free trial is long enough to see if the system works for you.

How does YNAB compare to EveryDollar or Quicken Simplifi?

YNAB is more comprehensive and behavior-focused. EveryDollar is simpler and ideal for quick tracking, while Quicken Simplifi offers broader financial snapshots. However, only YNAB uses the zero-based budgeting method and encourages long-term financial discipline.

Do I need to manually enter transactions?

While YNAB can sync with bank and credit card accounts, sometimes you need to manually enter transactions for accuracy or when syncing fails. Fortunately, this gets faster over time as YNAB learns your spending.

Yes! YNAB Together allows account sharing with up to five people at no additional cost, making it ideal for families or partners.

How does YNAB help me build an emergency fund?

YNAB’s philosophy of planning for less frequent expenses and recurring expenses encourages users to set aside money each month—building your emergency fund gradually and intentionally.

Is YNAB safe?

Yes. the app uses multiple security protocols, including bank-grade encryption. The app does not store your bank credentials and prioritizes user safety.

What’s the average savings for YNAB users?

According to the app, the average user saves $600 in their first two months and over $6,000 in their first year.

Final Thought

Budgeting is not just about tracking what you spend—it’s about being intentional with every dollar. The YNAB app won’t magically fix your finances overnight, but if you commit to the process, it will help you monitor your progress, reduce stress, and finally feel in control. That’s the kind of peace of mind that’s worth every penny.